Options Greeks, implied volatilities, and volatility surfaces for global exchange-listed options on equities, ETFs, equity indexes, and futures.

Options Greeks, implied volatilities, and volatility surfaces for global exchange-listed options on equities, ETFs, equity indexes, and futures.End-of-Day Options Greeks, Implied Volatilities & Volatility Surfaces.

Overview: In addition to end-of-day futures & options prices, DIH provides end-of-day options Greeks, implied volatilities, and volatility surfaces for global exchange-listed options on equities, ETFs, equity indexes, and futures. We include relevant security reference data for the options contract and underlying security.

Coverage: Our options Greeks, implied volatilities, and volatility surfaces cover over 10 million options and futures contracts and 10,000 issuers across over 25 countries and 45 exchanges.

History: We have historical data going as far back as 2017.

Updates: We update our data daily.

Delivery: You can receive our data in bulk files via download, S3 to S3, or on-demand via API.

License Terms: We license our data for either your internal use only or for display/redistribution to your clients. Unlike other data providers, DIH does not have purge clauses – so if you ever stop receiving data from us, you do not have to a ransom to keep the data you’ve already received and for which you’ve paid.

Pricing: Several inputs go into the pricing for our data. For example, do you want data for all available countries/markets, or a subset? How much history do you want? Do you want updates going forward? Contact us to learn more.

Why Firms Choose Our Options Greeks, Implied Volatilities & Volatility Surfaces.

Options prices do not always move in conjunction with the price of the underlying asset. So it is critical to understand the sensitivity of an option’s price to quantifiable factors. This is where options Greeks come in.

Options Greeks are calculated, and their accuracy is only as good as the model used to compute them, and the price and reference data that goes into the model.

Institutional participants in the derivatives markets choose to source their options Greeks, implied volatilities, and volatility surfaces from DIH for several reasons:

Proven Models – The models used to calculate our options Greeks, implied volatilities, and volatility surfaces have been thoroughly tested and vetted

Exchange-Sourced Raw Data – All of our options Greeks, implied volatilities, and volatility surfaces are calculated using raw price data from the exchange. The security reference data and corporate actions portions are sourced from the exchange and/or issuer.

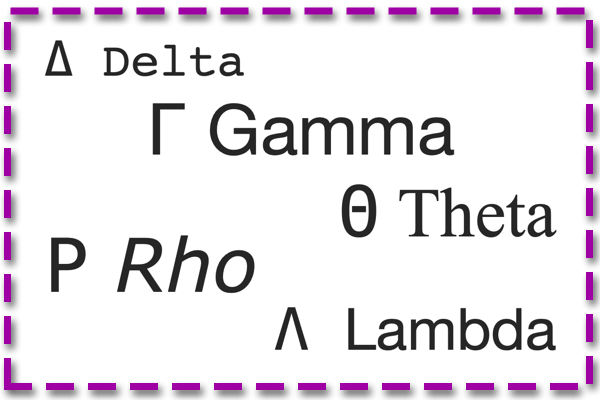

Variety of Greeks – We offer more than just the standard Greeks of delta, gamma, vega, theta, and rho. We also offer lambda, vanna, volga, spped, charm, color, zomma, and veta.

Geographic Coverage – We offer options Greeks, implied volatilities, and volatility surfaces for over 10 million options and futures contracts and 10,000 issuers.

Complete & Accurate Data – To ensure the highest quality data possible, all of the closing prices, security reference data, and corporate actions that feed into our models are checked both algorithmically and manually reviewed before they are made available for download.

Flexible Licensing Terms – DIH licenses its options Greeks, implied volatilities, and volatility surfaces for internal use or for display/redistribution. We also do NOT have any purge clauses like many data providers. So if you ever cancel your subscription, you do not need to delete the data you’ve already downloaded.

Affordable Pricing – Despite the high quality of our options Greeks, implied volatilities, and volatility surfaces, we still try very hard to work within our clients’ budgets.

What’s Included in Our Options Greeks, Implied Volatilities & Volatility Surfaces.

We offer the following standard and exotic options Greeks:

- Delta – sensitivity of options price with respect to underlying price.

- Gamma – sensitivity of options Delta with respect to underlying price.

- Vega – sensitivity of options price with respect to volatility.

- Theta – sensitivity of options price with respect to time (per day).

- Rho – sensitivity of options price with respect to interest rate.

- Lambda (orelasticity) – percentage change in option value per percentage change in the underlying price, a measure of leverage, sometimes called gearing.

- Vanna – is a second-order derivative of the option value, once to the underlying spot price and once to volatility.

- Volga (vomma) – is the second derivative of the option value with respect to the volatility or the rate of change to vega as volatility changes.

- Speed – measures the rate of change in gamma with respect to changes in the underlying price. This is also sometimes referred to as the gamma of the gamma.

- Charm (delta decay) – measures the rate of change of delta over the passage of time. It is the delta decay per day.

- Color (gamma decay) – measures the rate of change of gamma over the passage of time. It is the change in gamma per day.

- Zomma – measures the rate of change of gamma with respect to changes in volatility.

- Veta – measures the rate of change in the vega with respect to the passage of time. It is the change in vega per day.

All of our options Greeks can be calculated based on one of three volatility measures: implied volatility, interpolated implied volatility, or a propriety ex-ante volatility.

Implied Volatilities

In addition to options Greeks, DIH provides implied volatilities, which can be used to build implied volatility surfaces, including:

- Closing implied volatilities

- Listed implied volatilities surfaces by contract: expiry, strike, and put/call

- Price-Relative (moneyness) surfaces: strike relative to the underlying price (100 = at the money)

- Delta-Relative surfaces: call-equivalent delta (50 = at the money)

Interpolated Volatility Surfaces

We also use our implied volatilities to build interpolated volatility surfaces.

- Interpolate volatilities using closing implied volatilities

- Price-Relative (moneyness) surfaces: strike relative to the underlying price (100 = at the money)

- Delta-Relative surfaces: call-equivalent delta (50 = at the money)

DIH can also use other surface estimation methodologies based on your specific requirements. Contact us to learn more.

Reference Data for the Options & Underlying Security

With our options Greeks, implied volatilities, and volatility surfaces, we include relevant security reference data for the options contract and underlying security, such as:

- Options root symbol

- Underlying ticker symbol

- Underlying issuer name

- Underlying ISIN

- Underlying security type

- Exchange code

- Currency

- Expiration date

- Days to expiration

- Contract size

- Exercise style

Who Can Benefit from DIH’s Options Greeks, Implied Volatilities & Volatility Surfaces?

Because options Greeks, implied volatilities, and volatility surfaces are critical to anyone participating in the derivatives markets, or managing positions in the underlying securities, a wide variety of firms rely upon DIH’s options Greeks, implied volatilities, and volatility surfaces, including:

- Investment banks

- Brokerage firms

- Hedge funds (systematic & non-systematic)

- Asset managers

- Proprietary trading firms

- High net worth investors

- Service providers (e.g. OMS, EMS, data vendors, etc.)

How DIH Clients Use Our Data.

Institutional investors use our options Greeks, implied volatilities, and volatility surfaces for various tasks, including:

- Running back-tests or simulations of trading strategies

- Generate risk and regulatory reports on portfolios of options and underlying securities

- Perform in-depth analysis of options positions

- Calculate the amount of dividend equivalent payment and delta test for the IRS Section 871(m).

No matter what the use case, having accurate options Greeks, implied volatilities, and volatility surfaces is important.

Flexible Updates & Delivery.

Our options Greeks, implied volatilities, and volatility surfaces are updated on a daily basis.

You may customize our options Greeks, implied volatilities, and volatility surfaces to best suit your needs. For example, specify the instruments, exchanges, or countries from which you’d like to receive options Greeks, implied volatilities, and volatility surfaces. Also, choose how much historical data you’d like, and whether you wish to subscribe for updates going forward.

We deliver our options Greeks, implied volatilities, and volatility surfaces in bulk files. We can deliver files in various formats (e.g. CSV) via download or S3 to S3 transfer.